What The Optimist Can Learn From The Pessimist

Fixed Income Lessons and How to Apply Them When Investing in Equities

I spent three years of my career working in fixed income. I did everything from forecasting interest rates (an impossible job) to analyzing the junk bonds of a certain video game retailer, long before it became a meme stock. My true love was always equities, but circumstances in life gave me this opportunity. Nowadays I’m forever grateful as I came to appreciate its value when analyzing stocks and thus would like to share this with you.

In this piece, I will go over 3 Lessons I learned in fixed income that are especially relevant for equity analysts. I will break each one down in the context of bonds and offer suggestions on applying them when you’re looking at common stocks.

Lesson #1: Never Forget About the Downside

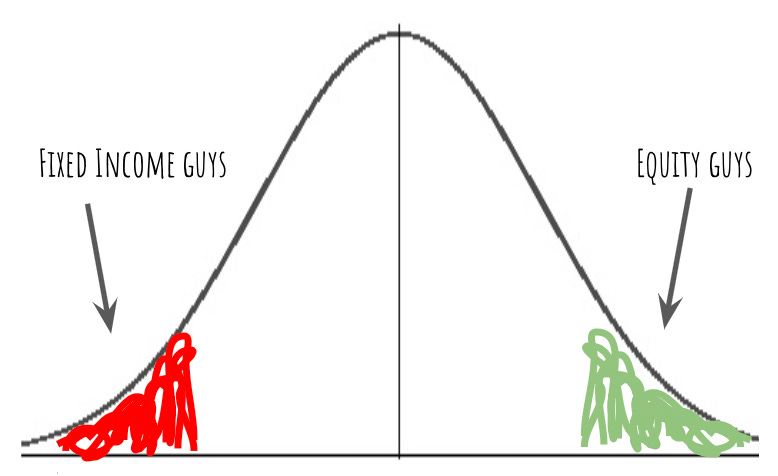

“Equity Analysts are optimists. Fixed Income Analysts are pessimists” —Unknown

The first question a credit investor asks is usually “What can go wrong here?” This is natural because you are lending money to the company, meaning at best you get paid back the principal plus a known interest rate, and at worst you lose most of your investment1. It’s one of those situations where you don’t want any surprises because they only come in the flavor of bad news.

As equity analysts, we tend to imagine the great growth prospects of the company, estimate the intrinsic value and how much upside there is from current prices. This makes our mouth water and that’s not an exaggeration: just the thought of making money activates the same regions in the brain as cocaine does. So it’s certainly tempting, but it also means that 90% of the time we’re focusing on what can go right. On the other hand, you’re completely caught off-guard when something like say, a pandemic, comes along and you never thought about what that could mean to your investment. How many DCFs have you seen with multiple scenarios and probabilities? Not many.

There are no absolutes in investing and the real world operates across a spectrum of probabilities of different outcomes. When we’re analyzing a stock, it’s human nature to focus on the optimistic scenario, which can be dangerous. The left side of the bell curve is sometimes just as probable.

What you can do about it: Stress Test Your Ideas

Here are a few ways you can Stress Test your stocks:

Make a list of potential events that would cause the company to lose value and the stock to fall: Earnings, revenue or user growth miss expectations. A large customer is lost. Hyper-inflation. CEO smokes weed on a Talk Show. Be exhaustive, you’ll be surprised what you can come up with. Try putting a probability around each one for any given year and how much value you think would be lost. This is more art than science, but for instance we know recessions happen every 7-10 years on average, global pandemics once every 100 years, etc. It’s ok to make wild guesses. Consider in which scenarios you would still hold the stock and in which you wouldn’t.

Compare your list to the “Risk Factors” section on the 10-K. It’s one of the most boring but also one of the most insightful sections. Highlight the ones you hadn’t thought of.

A filter I like to use is to ask myself: “Would I lend money to this company for 10 years at market rates?” You’d be surprised how many times the answer to this is

No, for a stock you thought about buying. Never a good sign ⚠️Look at the company’s bonds, where they are trading and what the price action has been. The bond markets sometimes sees something the equity investors don’t, and this can be very telling (remember they are pessimists). I’ve seen some pretty wild disagreements between a company’s stock and the bonds, such as a stock trading at 50x sales and the bonds at 50c on the dollar.2 This is not a sustainable relationship and something’s gotta give: either the bonds are insanely cheap or the stock is crazy overvalued (and at risk of bankruptcy). The inverse can also be true. AerCap bonds historically have traded at tight spreads (meaning investors think credit risk is low) while the equity constantly trades at single digit PE ratio and below book value.

Lesson #2: The Importance of Reflexivity

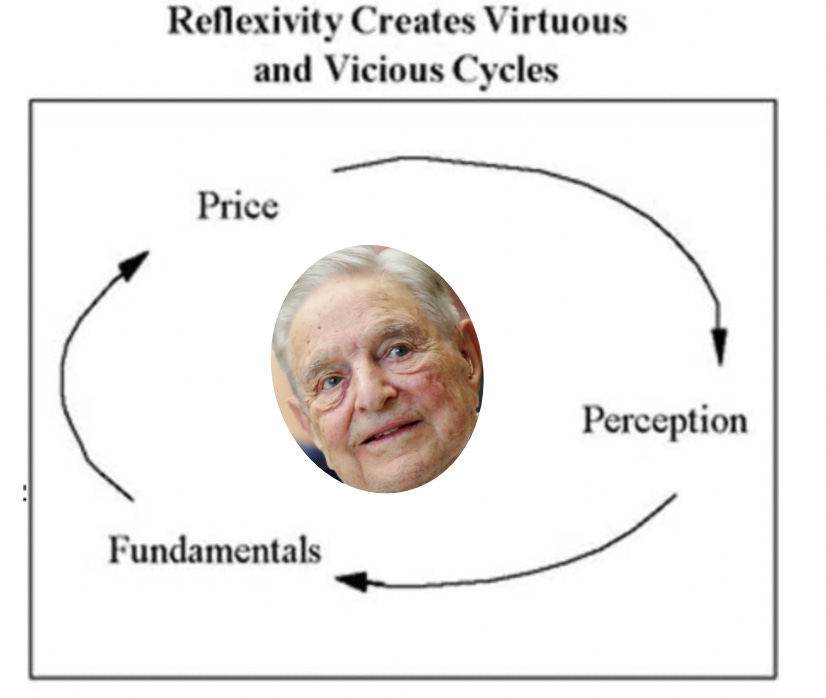

“The framework [Reflexivity] deals with the relationship between thinking and reality, but the participants’ thinking is part of the reality that they have to think about, which makes the relationship circular.” —George Soros

Reflexivity in investing is a concept that was popularized by George Soros3. It refers to the way reality (what most investors focus on) can be altered by the very perception of that reality, which means the participants’ thinking is just as important to consider as the facts themselves because they feed off each other🔄. An example of this is the Keynesian Beauty Contest where the best strategy is not determining who is the most beautiful contestant, but who you think people think is the most beautiful contestant.

In fixed income, if a company’s bond falls in price because credit investors think the company is struggling, when the bonds come due the company will have to refinance at much higher interest rates4 and may potentially default if it cannot afford those high rates. The negative perception investors have on the company may have altered the reality the company was facing.

This also applies to macroeconomics. In some ways, The Fed operates as a signaling agent by using various monetary tools to manipulate (i.e. calm down) investor perception and confidence towards the markets and the economy. Go back to June 2020: remember when some investors thought markets were a dead-cat bounce and another selloff would come, considering the dire economic situation? It certainly crossed my mind! Many of us forgot about reflexivity. Broadly speaking, market participants had a different view, we know this since the stock market and bond markets had already recovered almost all of their losses. What we missed was that the perception of investors had an impact on the actual reality, and surely enough economic recovery followed as confidence and sentiment came back thanks to that same perception. This is something fundamental investors often miss: sometimes there is value in the wisdom of the crowd and market prices can alter reality itself.

What you can do about it: Look at Prices and Sentiment

Try to understand the investor perception around the stock, what’s being priced in? Is the current prevailing sentiment optimism or pessimism? What happens to the company if the perception pendulum goes the other way? Will the company lose access to capital markets? Again, more an art than a science, but there’s value in thinking about these questions.

It’s best to find companies that are resilient instead of fragile, meaning less exposed and dependent to the vagaries of financial markets. Let’s take a closer look at a story from the Financial Crisis that offers some valuable lessons. Here we’ll see the difference between owning a resilient bank versus a fragile bank (as a side note: one was “expensive” and the other one “cheap”).

In mid-2008 the world was going through the worst financial crisis in memory. The banking industry was in a fragile state and the government had to step in to prevent a full meltdown by injecting capital into the banks, given the sector’s importance to the economy. J.P. Morgan was perceived to be a safer bank than Citi, which had more toxic assets (mortgages), higher leverage and as a result investors punished the stock more. This meant that Citi had to accept funds from the government at the worst possible time (through the TARP program) and shareholders were permanently diluted by essentially giving away 30% of the company to the Government5 at way below book value. Shares outstanding increased by a factor of 5X, which is why Citi stock still hasn’t recovered from pre-financial crisis levels and probably never will. On the other hand, JPM took the funds in the form of preferred stock, issued some equity to the public markets to prove to the government they had access, and promptly redeemed the preferred shares. The stock is up almost 360% since pre-crisis levels versus Citi stock down over 80%. Resilience and the perception of that resilience, is what saved J.P. Morgan while fragility and the market’s perception destroyed Citi’s shareholder returns.

Another final point on reflexivity: this is one of those times when selling a stock because it fell might make logical sense. If the company has a questionable capability to meet its obligations, and will struggle to raise cash quickly at decent terms because its stock and bonds fell off a cliff, it might be a good enough reason to take your money and run before it gets multiplied by zero. How many value investors would be averaging down in this situation? I’ve been guilty of this. I bet that money could have gone somewhere better when Citi started smelling like trouble in 2008 and it would also have saved you a lot of brain damage.

Please consider subscribing to FinChat to support The Sleepwell Strategy Substack and help keep the content free for everyone to enjoy! Sleepwell readers get a two-week free trial and 15% off paid-plans using the link below.

Lesson #3: Leverage Rarely Kills, Cash Coming Due Does

Sometimes you’ll hear a phrase like “The company is risky because it’s 5.0X levered!” High leverage above a certain threshold is concerning, but as we’ve noted, there are no absolutes in investing. What may be risky for a highly-cyclical dying video game retailer may be prudent for a mission critical software business that serves utilities and has a 98% retention rate. What really causes a company to file for bankruptcy is not leverage per se, but the inability to meet its obligations6. This is the difference between illiquidity and insolvency. You can be illiquid but perfectly solvent and you can be insolvent but perfectly liquid. The first one is about not having cash available today to pay for debts due today, the second one is about the size of your liabilities exceeding the size of your assets. One can kill you, the other not necessarily will.

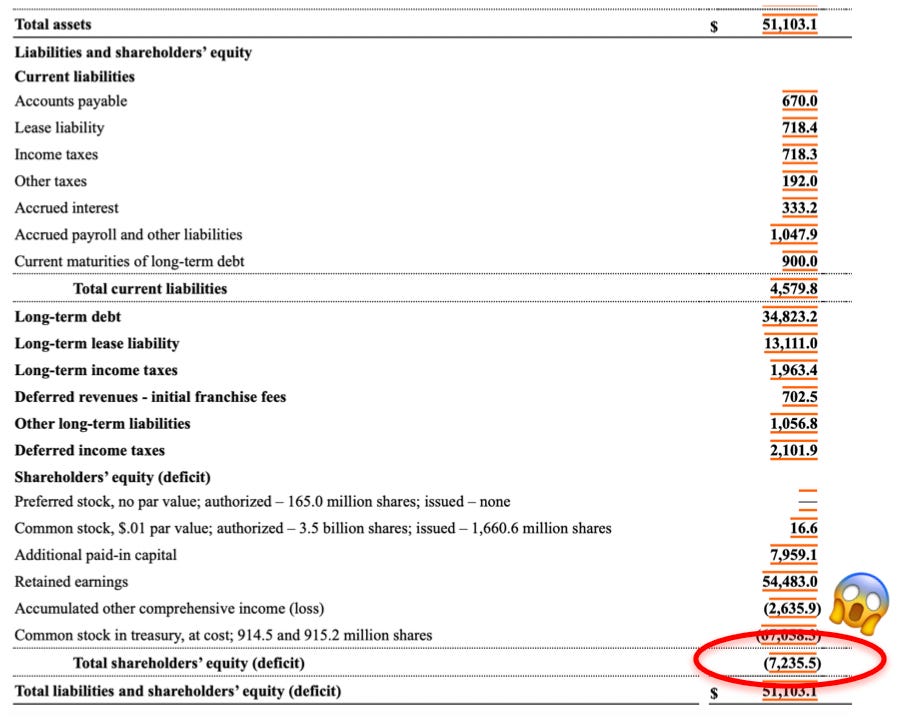

In the below figure, take a look at McDonald’s 🍟 balance sheet. Notice they have negative equity (assets<liabilities) mainly because they’ve bought back a lot of shares and don’t require much in capital expenditures. This isn’t necessarily bad, McDonald’s isn’t gonna default any time soon: they generate ~$6B of free cash flow every year and debt and lease obligations are covered by contractual rent payments under their franchisor agreements.

What you can do about it: Focus on the Maturity Wall

“Predictable income streams are much more valuable than volatile ones. Cause you can leverage them…” — John Malone

It’s no secret that John Malone is an expert and proponent of leverage. Charter, the second largest U.S. internet cable provider (which he owns part of), is no exception.

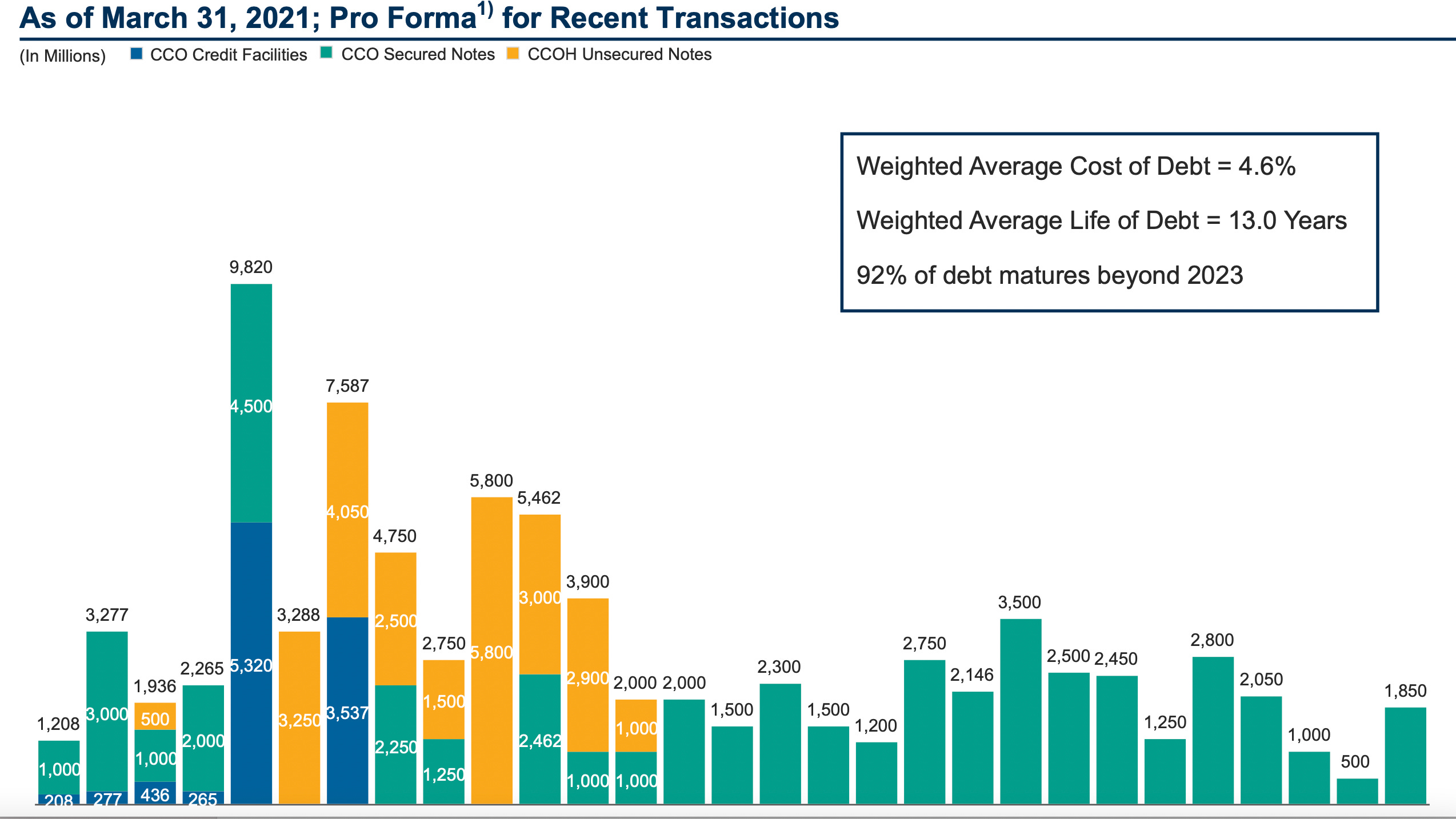

Charter’s leverage ratio (Total Debt/EBITDA7) is ~4.5X, which may sound high to some people and in fact it’s a High Yield rated company. But let’s take a look more closely at their maturity wall:

We can make two quick observations (assuming you know the company):

The debt is spread out pretty nicely, weighted average maturity is 13 years

Charter generates around $7-8B of predictable free cash flow which comfortably covers all of the upcoming maturities in the next 4 years, and likely will cover 2025 maturities (because it’s growing), also giving them plenty of time to refinance well ahead of the maturity date.

Not all companies provide this chart, but you can find some form of it in the 10-K under the Liquidity and Capital Resources (or Financial Condition) section, called either “Contractual Obligations” or “Commitments”. This will give you a pretty clear picture of the company’s contractual cash obligations for the next 5 years which you can compare to the company’s free cash flow generating ability8 and see if there are any large upcoming maturities in the near-term that may be difficult to meet. If this is the case, you are counting on their access to capital markets and become exposed to financial conditions and perception of the market (remember Reflexivity).

Bonding It All Together

Summarizing everything, the three Fixed Income tools for Equity Investors are:

Stress Test your ideas, be exhaustive

Look at the price and sentiment, find resiliency

Focus on the maturity wall and obligations, size it versus free cash flow

It should be pretty obvious that these are all connected with each other. I incorporate all three in my investment strategy by thinking a lot about the downside scenarios of my portfolio companies, having a good idea of what the market’s perception is and I try to pick resilient companies that have more than enough capabilities to meet their near-term obligations in different scenarios.

This helps me sleep better at night.

Some of it is typically recovered, known as recovery value and it’s usually around 30-40%

There’s typically an arbitrage opportunity here but that’s a subject for another piece

Lower bond prices equal higher interest rates: a 6% bond at 50c has a current yield of 12%

These were mainly in the form of warrants and Citi also issued equity to the public markets at an inopportune time

A company can also skip an interest payment which is a default, but usually it happens for the same reason: it knows it won’t be able to meet its near-term obligations

This is the traditional ratio used when analyzing credits, but there are many other options and many more conservative, such as using free cash flow. It’s also what credit rating agencies look at.

Some items here, like interest payments, are already subtracted from the traditional calculation of free cash flow, so make sure you don’t double count.

I am a big fan of reflexivity,not Easy to apply